Acceleration Clause: What is it and When is it Used?

Every contract is unique, but according to the Institute for Financial Literacy, 25% of mortgages now have acceleration clauses. These clauses protect lenders in times when individuals who have borrowed money cannot repay it or have somehow violated the terms of the contract. In this situation, the lender has the legal right to demand their loan repayment immediately.

If you are a lender and want to know more about creating lower-risk loan contracts, keep reading our article. We cover acceleration clauses, how they can protect lenders, and the types you can use.

We also explore acceleration clause examples and how you can take your documents to the next level by instantly generating them directly from Salesforce, using no code. So, stick around until the end.

Let’s get started!

What is an Acceleration Clause?

It’s a section in a promissory note that details how and when a lender can demand immediate repayment of a loan. This usually happens when certain conditions in an arrangement are unmet. For example, a lender can turn to the acceleration clause and follow its direction when the borrower has not made repayments, or the promissory note terms have been breached.

How Does an Acceleration Clause Help Lenders?

No one wants to think of a worst-case scenario. Still, an acceleration clause is added to loan agreements to protect lenders when a borrower does not make a scheduled payment or breaks a contract. In this case, the lender can use the acceleration clause to request that the full remaining amount of money owed be paid immediately.

Alienation Clause Vs. Acceleration Clause

We have already given you a definition of an acceleration clause. However, an alienation clause, also known as a due-on-sale clause, is also popular in contracts. The alienation clause is typically found in loan agreements, so it’s important to know about them as a lender.

The alienation clause allows the lender to request that the borrower pay back the full amount borrowed. This happens when the borrower wants to sell or transfer ownership of an asset related to the loan.

Since these clauses are popular in loan agreements, let’s check out their differences in more detail.

| Alienation Clause | Acceleration Clause | |

|---|---|---|

| Where are these clauses used? | The alienation clause is used in mortgages. | Lenders can use an acceleration clause in any loan. |

| What is the purpose of the clause? | It stops a borrower from transferring their asset to another person without the lender’s approval. | To protect the lender from a borrower who cannot repay the loan or violates the agreement. |

| Example | A mortgage with an alienation clause requires that the borrower pay the remaining loan balance if they want to sell their house. | A lender can activate the acceleration clause in an agreement when a borrower has missed many loan payments. At this point, the borrower has to pay the full balance of the loan immediately. |

Types of Acceleration Clauses

Acceleration clauses are added to loan agreements that take a long time to be repaid, such as:

- Mortgages

- Car Loans

- Business Loans

- Promissory Notes

Let’s look at the different types of acceleration clauses we can use in agreements.

1. Subjective Acceleration Clause

First on our list is the subjective acceleration clause, which allows the lender to force the borrower to repay the remainder of the loan immediately. However, in this case, the lender will choose to invoke the clause based on their subjective judgment.

Lenders will activate this clause whenever they feel the borrower’s financial health is low or they have failed to meet certain conditions.

2. Single Trigger Acceleration Clause

This next acceleration clause is found mainly in Executive Compensation or Stock Option agreements. A single trigger acceleration clause is invoked when a single event occurs, like when a company transfers ownership to a new entity. The purpose of this clause is to protect employees when their company is purchased or controlled by a new organization.

3. Uniform Acceleration Clause

This clause is used when a contract needs conditions for accelerating repayment for all lenders in the agreement. You will find a uniform acceleration clause in syndicated loans or agreements that are super complex. It’s needed because these types of contracts consist of many lenders supplying money to a borrower.

A uniform acceleration clause guides lenders in the event of a borrower being unable to repay loans.

4. Non-Uniform Acceleration Clause

Since we mentioned the uniform acceleration clause, we have to tell you about its opposite. The non-uniform acceleration clause allows multiple lenders to join an agreement which is essential for complex syndicated loans. Then, the lenders can individually demand repayment from the borrower just for their loan amount.

This means the collective group of lenders does not have to accelerate repayments simultaneously.

5. Instantaneous Acceleration Clause

Our last clause is not a popular term in the financial services or legal field. However, online readers do ask about this informal term. With an understanding of instantaneous acceleration in physics, we can guess that “acceleration” is measured at a specific time.

Therefore, we can deduce that business people might want to receive a full loan payment at a specific time and event. What are your thoughts on this term?

Acceleration Clause Examples

There are many examples of acceleration clauses, but let’s take a look at a simple and common use case.

Alex has lent money to an individual, but the borrower has now missed many payments. In this instance, Alex can turn to the acceleration clause in their agreement and use it to request that the borrower immediately pay the remaining amount of the loan and interest rates.

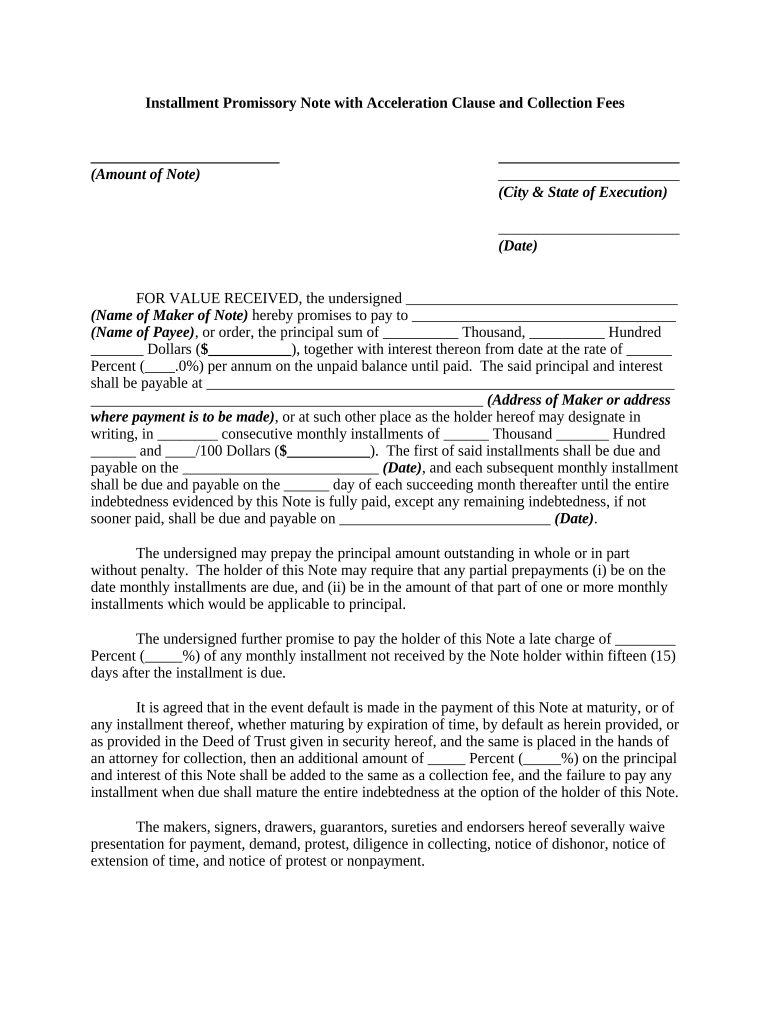

Pictures speak for themselves, so here is an example of an acceleration clause that can be referenced for use in the real world:

Wrapping Up Acceleration Clauses

And that’s all the information we have on acceleration clauses. Thanks for reading our article! We hope you now understand this topic better so you know your rights as a lender.

You totally have options to speed up the repayment process when a borrower defaults on their promise or violates terms in a loan agreement.

Generate Documents at the Click of a Button with TITAN Doc Gen

By the way, if you are looking for unbeatable document solutions, we suggest you check out Titan. Our no-code platform gives you point-and-click tools to generate documents, like agreements, instantly from Salesforce.

Imagine all those contracts and promissory notes containing acceleration clauses. Titan can help you create them with pre-filled Salesforce data and a single button click. Sending loan agreements to borrowers or key stakeholders for electronic signing can also be easy with Titan.

So, let’s quickly take a look at the features you get when you integrate TITAN document generation in Salesforce:

- Build custom contracts, loan agreements, promissory notes, and more from Salesforce without code.

- Read any field from Salesforce objects and reports, then display the data in any format.

- Add interactive functionality to your documents to write data to Salesforce objects.

- Titan allows you to work with standard and custom Salesforce objects.

- Map barcodes and QR codes from your documents to Salesforce for paperless payments and transactions.

- Automate any process using no code to streamline complex document flows between lenders and borrowers.

- Generate loan agreements and electronically sign them seamlessly using Titan’s drag-and-drop builder.

- Store documents in various locations, like Salesforce, Google Drive, or Box.

- Your documents have end-to-end security and comply with HIPAA, ISO, SOC 2, GDPR, and other leading frameworks.

- And more!

Personalized Salesforce Solutions with Titan

These are just a few things you can achieve with Titan in your software stack. Contact us through our social media channels below for a full feature list. We would love to hear from you.

See you soon.

Disclaimer: The comparisons listed in this article are based on information provided by the companies online and online reviews from users. If you found a mistake, please contact us.

You might be interested in

Writing Your First Notarized Letter Like a Pro

How to Remove Track Changes in Word

Signee Vs. Signer Vs. Signatory: What are They?

All-in-One Web Studio for Salesforce